Summing up The way to get a house Collateral Loan

Trying to get a property Collateral Financing

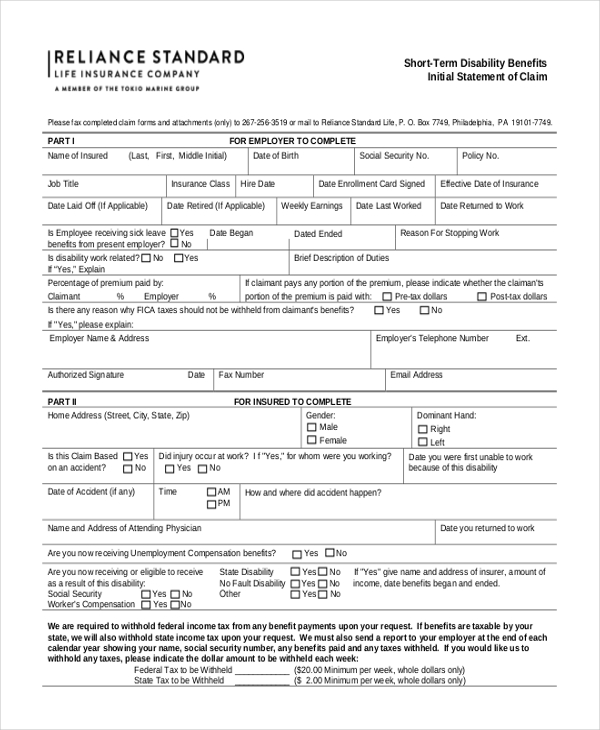

A property collateral mortgage try an additional mortgage. And you are clearly planning to come upon similar management needs to those you confronted after you taken out your primary home loan.

If you would like your finances in the future, it is advantageous to collect most of the records their lender’s browsing want before applying. Experian has a checklist.

Of course, if you’ve go out before you can want to pertain, you could test to gain access to most useful financial contour. Which ought to change your possibility of taking acknowledged and may also secure your a lower interest.

Such as, settling the mastercard stability will be improve your credit history and inch your DTI all the way down. You might improve your residence’s worthy of of the tidying within the indoor and you may additional (just cleaning, paint, and lesser solutions) and you can putting some turf due to the fact attractive that one may.

Household Equity Financing Assessment

Typically, lenders almost always need an enthusiastic appraiser so you’re able to scan your property and you can promote an effective valuation. But COVID-19 made in-person visits undesirable.

- Drive-because of the appraisals Where in fact the appraiser does not come into the that can perhaps not move out regarding his auto

- Pc appraisals The spot where the appraiser never ever will leave the office and you can from another location inspections on the internet provide such as for example taxation information in addition to Mls

- Automated Valuation Patterns (AVMs) Where the whole thing’s accomplished by pc having fun with sophisticated formulas. If you would like the gory technology info, look at this.

AVMs are inexpensive and easy. And your financial tends to be proud of you to definitely, specifically if you keep numerous collateral while having a low LTV. Nevertheless they never generally take membership of all the have and you may finishes which make your residence special which more valuable.

Thus, if you’d like a loan that have an excellent borderline LTV or you has actually a reduced credit history, you’re happy to inform your lender you’ll be able to pay the price of the full, conventional household appraisal. Based on HomeAdvisor, that has been, at the beginning of 2022, contained in this a frequent listing of $313 and you will $420 to own an individual-household members hold.

Refused? Choice so you can House Collateral Money

Because the family equity fund are secure debts, they generally provides dramatically reduced rates than just unsecured borrowing from the bank. Thus do not be defer if one bank refuses the application. Is actually most other, more sympathetic of these.

But what goes if you have kissed the family collateral frog you find and so they all turned over to become wholly unroyal amphibians? You may be from of options. Listed here are around three:

- Unsecured loans Talking about the same as domestic equity funds, except these include unsecured (no LTVs) and you will generally have higher rates. But not, set-up costs are usually zero.

- FHA 203K Rehabilitation financing That it merely work if you prefer a property guarantee mortgage so you can financing a property update endeavor. It is simpler to be considered and you may most likely rating a decreased price. However, closing costs may be higher.

- Loans government plans (DMPs) If you wish to obtain so you’re able to consolidate your financial situation. Throughout the years, you might find your own DTI fall and your credit score go up. Attempt to like a reputable spouse.

Think hard on how you just do it. Having your app rejected might possibly be a red flag which is caution one review your financial things. So simply take you to seriously.

Basically, American people was going home based collateral so you’re able to an unprecedented extent. Here are some surprising analytics out of CoreLogic, a buddies that usually inspections and you can analyzes family guarantee. From the history quarter from 2021:

CoreLogic investigation reveals You.S. homeowners with mortgages … have experienced their equity improve by all in all, more $3.dos trillion because fourth quarter out-of 2020, an increase from 29.3% 12 months over 12 months.

свежие записи

-

12 нояб. 2024

12 нояб. 2024Flamenco Roses Slot Auswertung 2024 I Greentube